Paying Less Taxes: How Internationally Organized Crypto Companies Pay Less Taxes

This is some learnings around how complicated corporate structures take advantage of tax havens and "Foreign" revenue.

Hello Professional Curious one!

Today I’m going to get extremely nerdy.

More nerdy than Crypto.

I’m going to talk about Finance, Tax, Business Structures, and of course Crypto.

Specifically I’m going to talk about how companies that organize themselves in such a way that owning a foreign company reduce their tax burden.

This piece is inspired by my thoughts on blockchain are payment roads, and how the entire blockchain ecosystem is basically geographically anonymous by design.

Enjoy the read!

Happy Thanksgiving!

p.s. I left a recipe for you at the end to save you.

In Case You Missed It

Sections You Can Skim To

A Simple Company Structure

Tax Havens

Allocating Intangible Assets

Proving Foreign Income

Taking the FDII Deduction

Applying the FDII Deduction

Disclaimer

What I’m about to tell you should not be considered legal, financial, or in anyway, business advice for you and your operations. Seek advice from your own professionals and consult your own experts.

I’m just a guy poking at things.

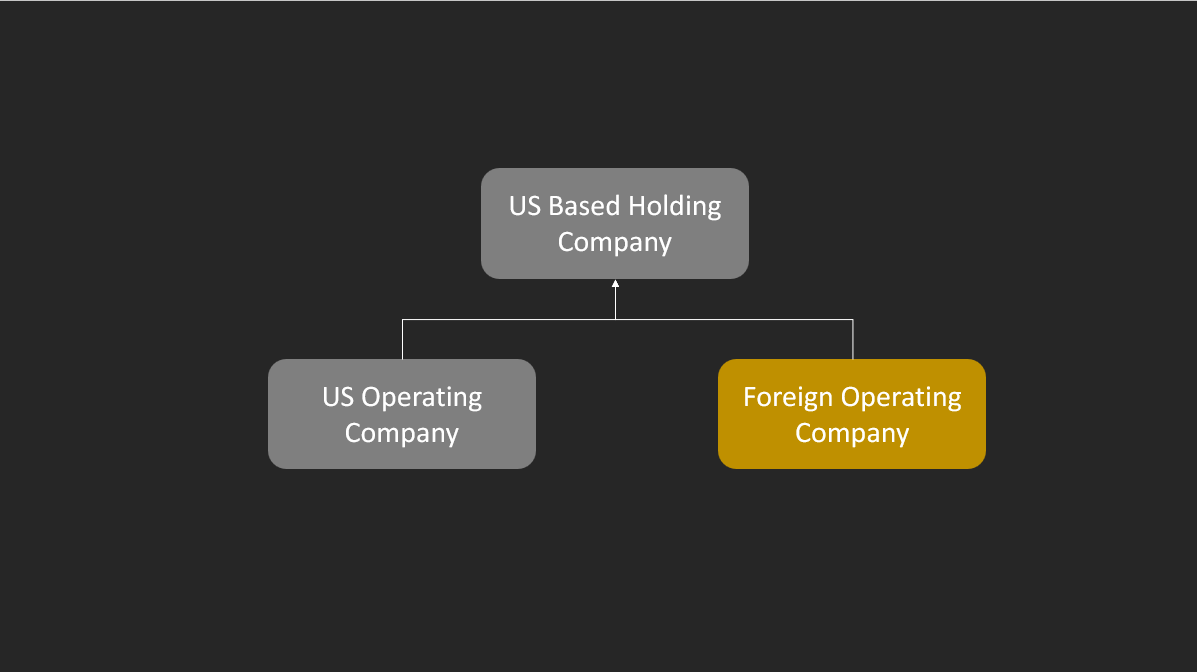

A Simple Company Structure

TL;DR: Let’s own a Foreign Company.

U.S. Companies take advantage of the U.S. Tax Code by creating several other companies, all owned by the same holding company. A basic example is shown above.

You have the U.S. Based Holding Company, of which everything related to the company, including all owned things, consolidate and roll into.

Then you have the US Operating Company which is used to manage US Operations including hiring, payroll, decision making, etc.

Sometimes, this foreign company is actually the parent company (everything consolidates to that foreign company). Sometimes its a US Parent company.

It depends.

Companies create a foreign operating company to handle business presumably outside of the US. I kid. It’s mostly for tax haven.

Tax Havens

TL;DR: Everyone loves the Caymans. Or Seychelles. Or Panama.

The British Cayman Islands, as well as a few other islands, have incredibly lax tax laws. In fact, it’s so favorable that there are 117,000 companies registered in Cayman including Binance.

Tax havens offer an incentive (less taxes paid) on revenue earned from that haven, and/or another country (like the United States) offers tax benefits from foreign earnings in these havens.

Without getting into the details, for the purpose of my original example in this post - that of Foreign Derived Intangible Income - let’s assume we have a US Parent Company, and it wholly owns a Cayman Company, Our Foreign Company.

So what’s next?

Allocating Intangible Asset

TL;DR: Feels like a loophole.

At this time, Crypto is considered an intangible asset, joining the likes of intellectual property, goodwill, brand recognition, patents, trademarks, and copyrights. (Note: It’s common for a foreign entity to license, or be licensed, some form of IP, Patent, or Trademark, thus reducing tax burden).

Taking advantage of the Crypto Classification as an Intangible Asset, the argument is then made that all income made off of Crypto is Intangible Asset Income. This is an argument that is made and decided at inception of the company, and can’t be retroactively applied.

The question is, from where is that Intangible Asset Income earned?

In comes the Our Foreign Entity.

We can take a position that all of our Crypto earnings are earned first through Our Foreign Company, before its passthrough into our US Holding Company / US Operating Companies.

This position is only defensible when: Our Foreign Company earns revenue from other Foreign Companies

It does not work when: Our Foreign Company earns revenue from U.S. Companies or U.S. Based Activities.

The question then becomes, how do we prove that Our Foreign Entity is deriving income from Foreign sources?

Proving Foreign Income

TL;DR: Tax positions are basically a game of “how defensible is your argument”.

If Our Foreign Entity enters into financial sales agreement with another foreign company not from the U.S., well congratulations: You just earned yourself some bona-fide intangible asset income from your foreign entity.

Otherwise known as Foreign-Derived Intangible Income.

There are several ways to go about achieving this goal:

Foreign Company, Foreign Business: We have Our Foreign Company directly do business with another Foreign Company, knowing full well they are acting as an intermediary. If we have a lot of Crypto Tokens (like a shit ton), we can contract with behind the scene Market Makers such as Amber Group, a company headquarter in Hong-Kong.

We Avoid Companies That Have Know Your Customer Compliance: I suppose one can make the argument that you didn’t know you were selling to a U.S. company, and thus your income isn’t U.S. derived, is an argument. And I suppose you can simply avoid all the exchanges and institutions that have any level of compliance.

Lack of Blockchain Customer Information: There is no KYC information on-chain - the current way crypto transactions are setup is that you have no idea who is on the otherside. It’s all anonymous, and thus, unprovable to be in the US or not in the US. So hop into a DEX, and sell your Crypto. But the question remains - how will you “off-ramp”, which is to say, how do you convert your crypto into fiat that isn’t tied to a U.S. Source? Get creative, you’re already here.

Big trades and deal can happen off-chain: B2B Deals such as partnerships, loans, financing, and market making deals happen legally outside of the U.S. An example would be something like Kraken paying Our Foreign Company $25k per Month to advertise their platform.

Now that we’ve established Our Foreign Company and where we earn our Foreign Income, now we can talk about the Foreign-Derived Intangible Income Deduction.

Taking the FDII Deduction

TL;DR: Take a 37.50% Deduction!

Skipping forward the semantics of what else you can do, let’s start talking about how Foreign Derived Intangible Income works to the benefit of the US Holding Company. This entire FDII Deduction comes from this: IRC Section 250: Foreign-Derived Intangible Income (FDII)

I read and executed this document and I’m here to tell you this:

You can deduct 37.50% of your Foreign-Derived Intangible Revenue off your total consolidated revenue, leaving you with a smaller taxable revenue amount.

Yes it stacks with other tax voodoo magic that’s possible.

It does not stack with R&D. If you claim R&D Credit, that portion is mutually excluded from any FDII benefit whatsoever.

Here’s how it works:

All revenue earned by Our Foreign Company, that can prove it earned its revenue through actual foreign business, can qualify to deduct 37.50% of all of its Foreign Revenue from its total revenue. Only if you make revenue; losses don’t count.

Let’s learn it using big league numbers:

Rolling forward our US Holding Company with our US Operating Company (where you work at, probably) and Our Foreign Company based in Cayman.

Let’s imagine our entire company earned $100,000,000 in revenue, and that 100% of it was made strictly via Crypto-Only based sales transactions.

Let’s see how this $100m gets taxed without, and with, the FDII Deduction.

Applying the FDII Deduction

TL;DR: Save up to ~8% on your tax bill.

Without FDII Deduction

Note: The below example is a simplified example and does not consider other things companies do such as deduct the cost of goods, cost of operating the business, depreciation, etc. This is strictly a revenue & tax example.

Total Revenue: $100,000,000

Taxable Revenue: $100,000,000

Assume 21% Corporate Tax Rate

Tax Bill: $21,000,000

Effective Tax Rate: 21%

This is the amount the company actually feels.

In this scenario, we do not have the benefit of FDII.

With FDII Deduction

Below example assumes 100% of all revenue is crypto and “Held” first by Our Foreign Entity in Caymans, prior to it passing through to US Operations.

Total Revenue: $100,000,000

FDII Deduction: -$37,500,000

(37.50% of $100m)

Taxable Revenue: $62,500,000

Assume 21% Corporate Tax Rate

Tax Bill: $13,125,000.

Effective Tax Rate: 13.125%

We have a reduction in our effective tax rate, what we actually pay. Deduction comes after EBITDA, or Operating Income.

Comparing No FDII and FDII

No FDII Deduction: $21,000,000

With FDII Deduction: $13,125,000

Net Saving: $7,875,000, or 7.87% ←- pays for my salary, I suppose.

Note: You won’t be able to claim 100% of your FDII as a deduction as you first need to also reduce your Foreign Revenue by the cost of operations, whether its by US Personnel or Foreign Personnel.

Note2: FDII only qualifies for when you have a gain, or profit, on your foreign sales. Losses are excluded because these are represented as reductions in Operating Income.

Note3: Realistically, its just cost accounting and tax accounting came together.

The Big Assumptions

This entire thing only works if you have:

Solid Financial Record Keeping

Solid Legal Documentation

Solid Finance and Accounting Team

Solid Tax Provider and Tax Lawyer who can argue cases

Hope you enjoyed this piece.

It gets far worse if you make NFTs for example and start to consider what the cost-basis of the company is and what the value of our unsold pictures are.

Cheers!

Don’t know what to make for Thanksgiving?

Make Kenji Alt-Lopez’s Crispy Potatoes. It’ll cost you less than $10, and feed everyone easily. Buy a bag of Yukon Gold Potatoes and get to work.